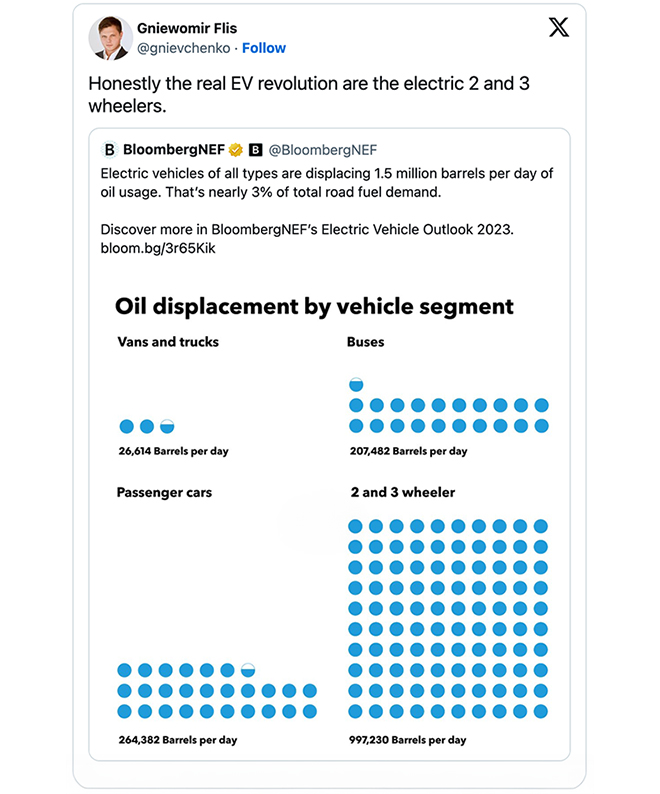

| | Climate change comes home As we've been reminded again and again, weather-related disasters—from devastating fires to supercharged storms and deadly floods—are becoming both more frequent and more extreme as global temperatures rise. And homebuyers are taking notice. A survey this month by real estate marketplace Zillow found that " more than 80% of home shoppers consider climate risks when looking for a new home," a sensible development considering that home equity accounts for most of the middle class's wealth. But while buyers may be taking the risk of flood or fire into account when looking at specific properties, they aren't necessarily moving to safer areas: Zillow found that more than 75% of those surveyed planned to stay in locations with similar or even greater risk. An impending insurance crisis may convince them. Across the country, home insurers—seeking to preserve profits and avoid costly payouts—are pulling out of markets hit hardest by climate-related disasters. In California, State Farm and Allstate have stopped writing new policies, while USAA has implemented a scoring system based on wildfire risk. Hurricane-battered Florida has seen the same pullback, with many of those who can still find coverage paying premiums of more than $10,000 a year. When private insurers leave, the government is often the insurer of last resort, although chronically underfunded federal programs like the National Flood Insurance Program aren't sustainable solutions either. The crisis is unlikely to be resolved any time soon and will probably get worse as more of the country is affected by extreme weather events. For now though, homeowners are largely staying put. Wharton economist Benjamin Keys points out in a Q&A with PennToday that climate risk just isn't priced into the current insurance model. We're not seeing the price signals that we need to change behavior. What that means is that builders, for instance, are getting the wrong signals; they're getting the signal that we should be building more in coastal Florida, building more in Arizona. When, in the long run, we know that there are communities that are not going to be sustainable without dramatic changes to how we live. So, there's a disconnect when we see both rising climate risk and rising house prices in these areas. + Relocation brings its own set of challenges, particularly for those with lower incomes. + Auto insurance is having a disaster-related crisis of its own. | | | | | Depave paradise and get rid of the parking lot Our changing climate won't just dictate where we live, but how. In a hotter world, everything we can do to lower temperatures is critical, particularly in large population centers. The Depave movement proposes a relatively simple fix with a big payoff: tear up asphalt and plant some trees. We've mentioned the heat island effect before; in a nutshell, pavement absorbs and retains heat, and heavily paved locales can reach temperatures that are nearly 10 degrees hotter than a city's average. And these neighborhoods are often low income, with more residents of color—a consequence of racist housing policies. Less pavement and more green spaces means a cooler city, and one that's less prone to flooding. Not to mention knock-on effects like better air, less noise, and healthier residents. + Another good idea: planting tiny forests. | | | | | Things are looking bright for EVs A recent UN assessment warned that we have "a rapidly narrowing window" to cut emissions and avoid the worst of climate-related disasters. There's much left to do, but amid the missed goals and broken promises, there's been some good news too. According to the US Energy Information Administration, "the United States added 6.4 gigawatts (GW) of small-scale solar capacity in 2022, the most ever in a single year ." And the energy research and consultancy group Wood Mackenzie estimates that the country's total annual renewable energy capacity could reach 110 gigawatts in the next decade thanks to the Inflation Reduction Act. One of that act's key goals is getting more people into electric cars. And despite some stumbles, interest in EVs is relatively high. BloombergNEF's latest Electric Vehicle Outlook report shows EV adoption rising throughout the world. US consumers on the whole have been reluctant to swap their gas-powered vehicles for EVs. But as Shannon Osaka and Emily Guskin note in the Washington Post, last year the country finally hit a key milestone —the so-called "tipping point," when electric vehicles accounted for 5% of all new car sales. If the US follows the trend established by EV leaders like Norway, adoption should rapidly increase in the years to come. Time will tell if this holds true, but for an optimistic case, look to California, which reached the 5% tipping point in 2018. Californians were early EV adopters, and in the past five years annual sales have exploded from 2% of the new car market to 22%, with the state on track to reach 26% by 2026. + Electric cars are old news now that electric air taxis are on their way. United Airlines and Eve Air Mobility have announced a prospective program in the San Francisco Bay Area. And Steve LeVine has documented "the U.S.-French race to electrify the skies above the Olympics" over at the Information. + And soon you'll be able to take an electric commuter ferry around the Orkney Islands. + But as Gniewomir Flis noted on X, the EV segment with the most potential is the humble motorcycle. | | | | | | | | | | —Tim O’Reilly and Peyton Joyce | | | |

Комментариев нет:

Отправить комментарий

Примечание. Отправлять комментарии могут только участники этого блога.